Post-Draft Extensions: When Extensions Align With Winning Windows...And When They Don't

Three recent deals riding positional market booms and how they look with context.

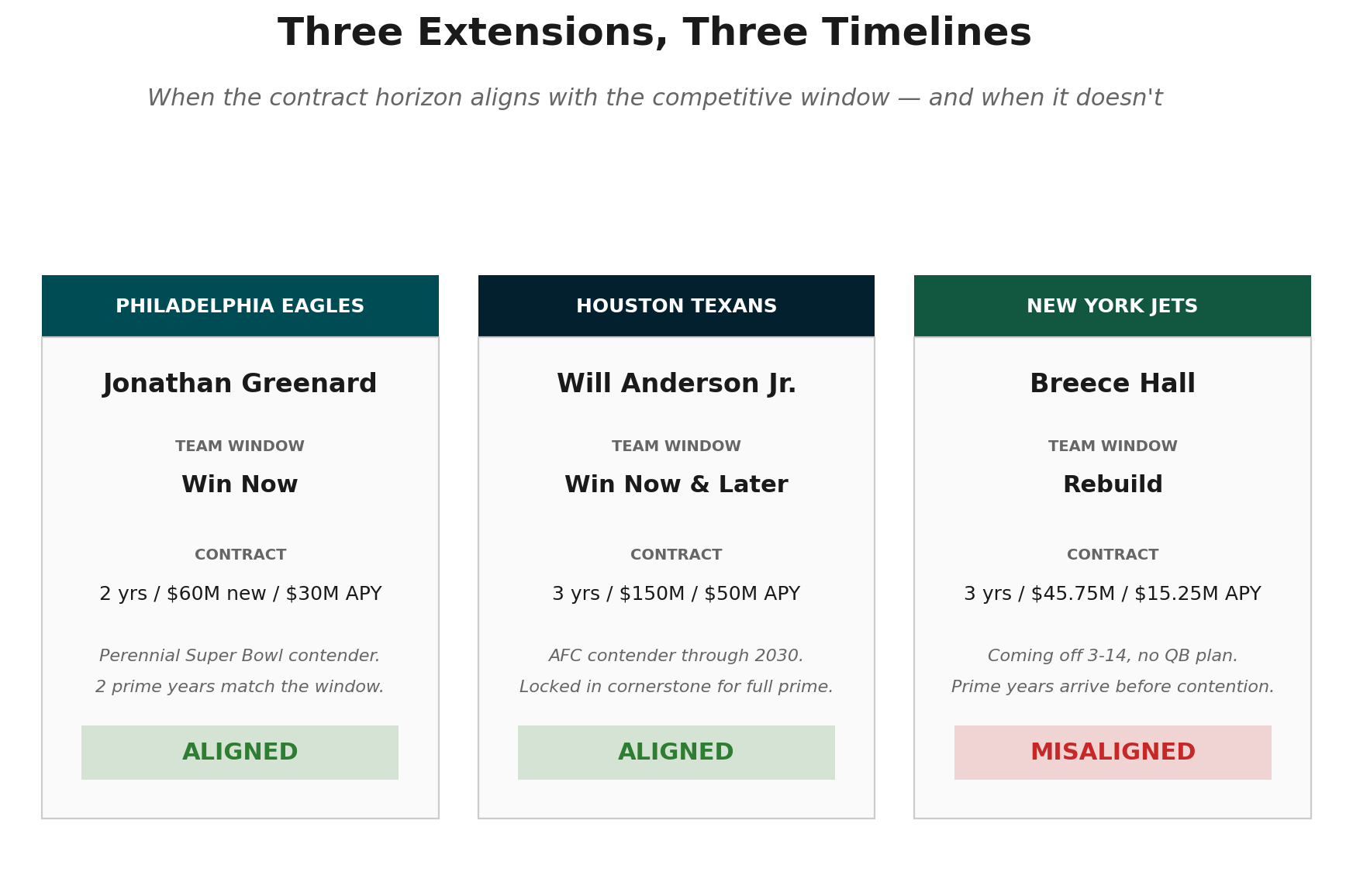

Over the past three weeks, three teams paid a premium to lock up players they wanted to keep. The Eagles traded two third-round picks to pry Jonathan Greenard out of Minnesota and immediately signed him to a $98 million extension. The Texans gave Will Anderson Jr. the largest non-quarterback contract in NFL history. And the Jets made Breece Hall the third highest-paid running back in football.

One of these deals isn’t like the others. It just isn’t the one you think.

Look at those deals on the surface and the Greenard transaction looks the worst by a wide margin, a 29-year-old edge rusher coming off shoulder surgery, signed to an above-market contract, with two picks given up just to acquire the right to write that contract.

The lens that sorts them is simple: does the contract horizon align with the team’s competitive horizon? A four-year deal that buys a player’s age 25 through age 28 is a different deal depending on whether you’re a perennial Super Bowl contender, an AFC contender with a quarterback still on a rookie deal looking to compete for years to come, or a 3-14 team in the second year of a new regime’s rebuild. The cap is finite. The window is finite. The question every front office has to answer is whether they’re spending the player’s prime in the years that matter for them.

That framing also sorts the analytical work. I have, at times, been too focused on value in a vacuum and not applied the proper context of marginal wins and where teams are on the winning curve. That matters. A market overpay during a championship window is a price of doing business. A market overpay during a rebuild is a tax on a future that hasn’t shown up yet. The dollars are the same. The fit isn’t.

Two of these three teams answered the fit question correctly. The one that didn’t is also the one that paid the smallest absolute premium, the player most generally regarded as a star at the prime of his career, on the contract that drew the least scrutiny when the news broke. That’s what makes it the misaligned deal of the spring. The math is fine. The math is just being applied to the wrong calendar.

Jonathan Greenard, Philadelphia Eagles

The team timeline: The Eagles are a perennial Super Bowl contender. They've made the playoffs in five of the last six seasons, won the conference twice, and won Super Bowl LIX two years ago. Jalen Hurts is in his prime. The skill group is stacked, even as they are set to trade away A.J. Brown. The offensive line is still quite strong, the defense returned most of its core.

Yes, general manager Howie Roseman lost Jaelan Phillips to Carolina in March, leaving a hole opposite Nolan Smith on the edge. The window is right now, and the next two years matter more than the four after that.

That’s the lens you have to apply to the Greenard transaction, because the surface read makes it look bad in every direction.

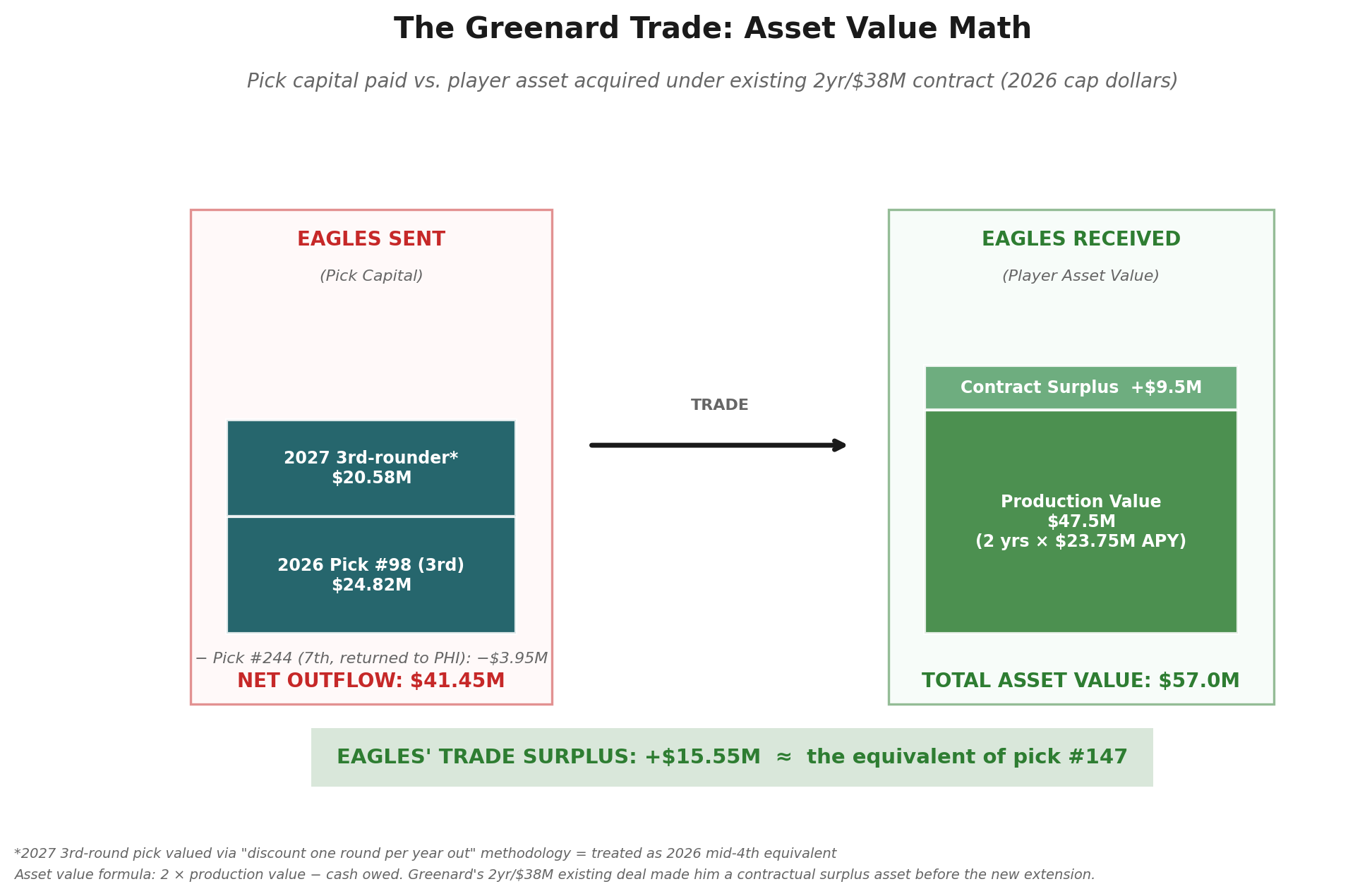

On April 24, in the middle of the second day of the NFL Draft, the Eagles traded picks 98 (a 2026 third rounder) and a 2027 third-round pick to Minnesota in exchange for Greenard and pick 244 (a 2026 seventh). They then signed Greenard to a two-year, $60 million extension with $50 million guaranteed. That put Greenard under contract with the Eagles for a total of four years and $98 million.

His extension APY, $30 million, tied him for the eighth highest amongst all edge rushers. He would fall to tied for ninth highest in short order. More on that later. But this is big money for a 29-year-old pass rusher who finished the 2025 season on injured reserve after shoulder surgery, after recording 3.0 sacks in 12 games on a Vikings defense that was supposed to ride him into a deep playoff run. Plus, two third-round picks given up to acquire him.

Walk through the analysis layer by layer and the deal looks better at every step.

The Trade

Run the picks through my published draft pick value chart, inflated to 2026 cap dollars (the cap rose from $255.4M in 2024 to $301.2M in 2026, an inflation factor of 1.18):

2026 Pick #98 (3rd round): $24.82M

2027 3rd-round pick (treated as 2026 mid-4th equivalent under the future-pick discount, which adjusts a year-out pick down one round): $20.58M

2026 Pick #244 (7th, returning to PHI): -$3.95M

Net pick capital from Philadelphia to Minnesota: $41.45M.

Greenard had two years remaining on his old contract at $38 million in cash owed to him. By my draft value chart, the trade valued him correctly based on his existing deal.

But when you look at his market value you start to see that Roseman and the Eagles got a discount on the pass rush juice they know they need. My projection models have his value at a $23.75 million APY and $47.5 million overall. Add in his contractual surplus value - his on-field value minus the cash he is owed - and his actual value as a trade asset is $57 million. The Eagles made out by about $15.5 million, or the equivalent of pick 147.

The Extension

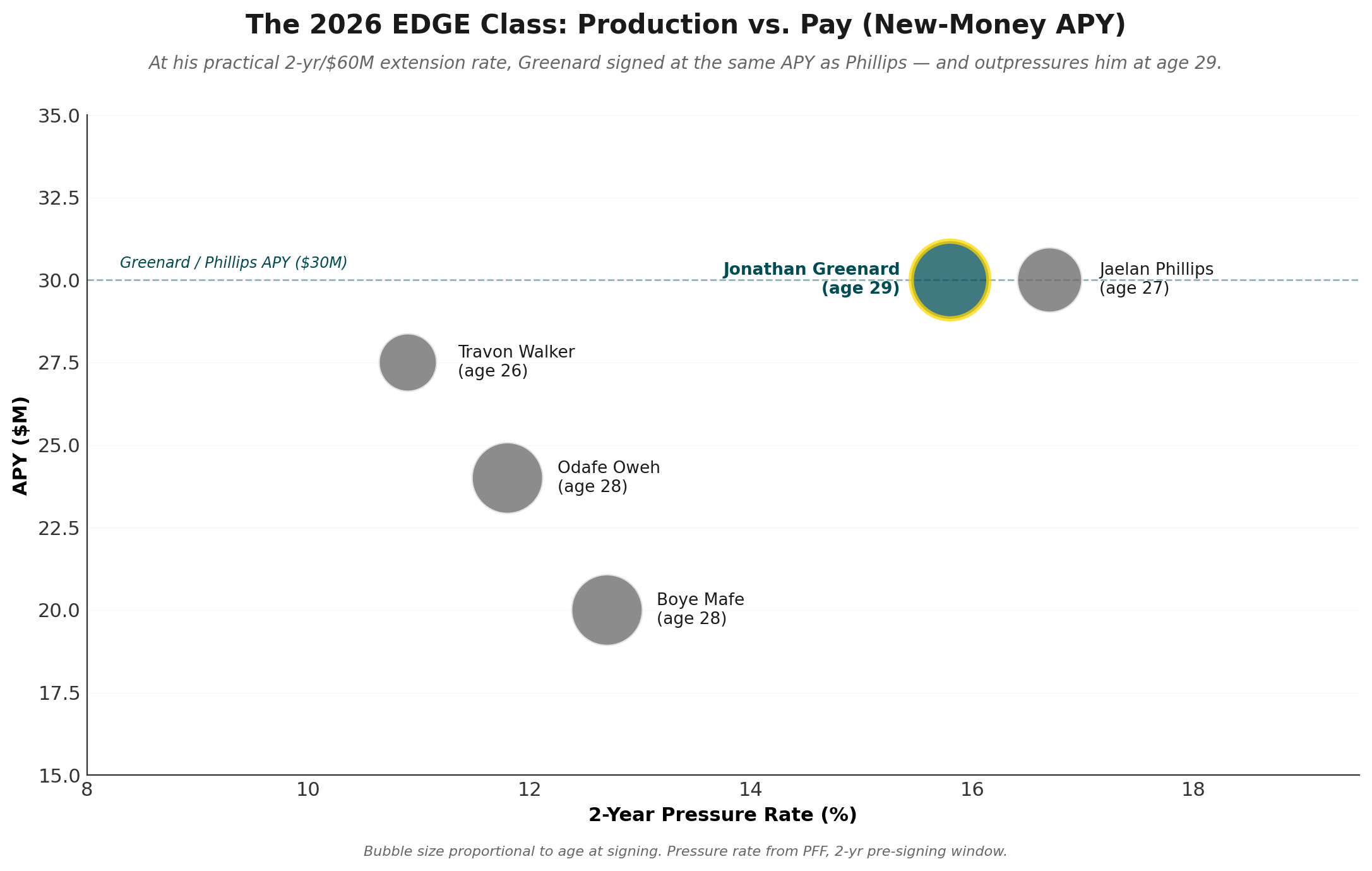

The contract that came on top of the trade is the part that initially looks the most damning. Two years, $60 million, $30 million APY and 83% fully guaranteed at signing for a 29-year-old coming off shoulder surgery.

Compare it to the rest of the 2026 EDGE class:

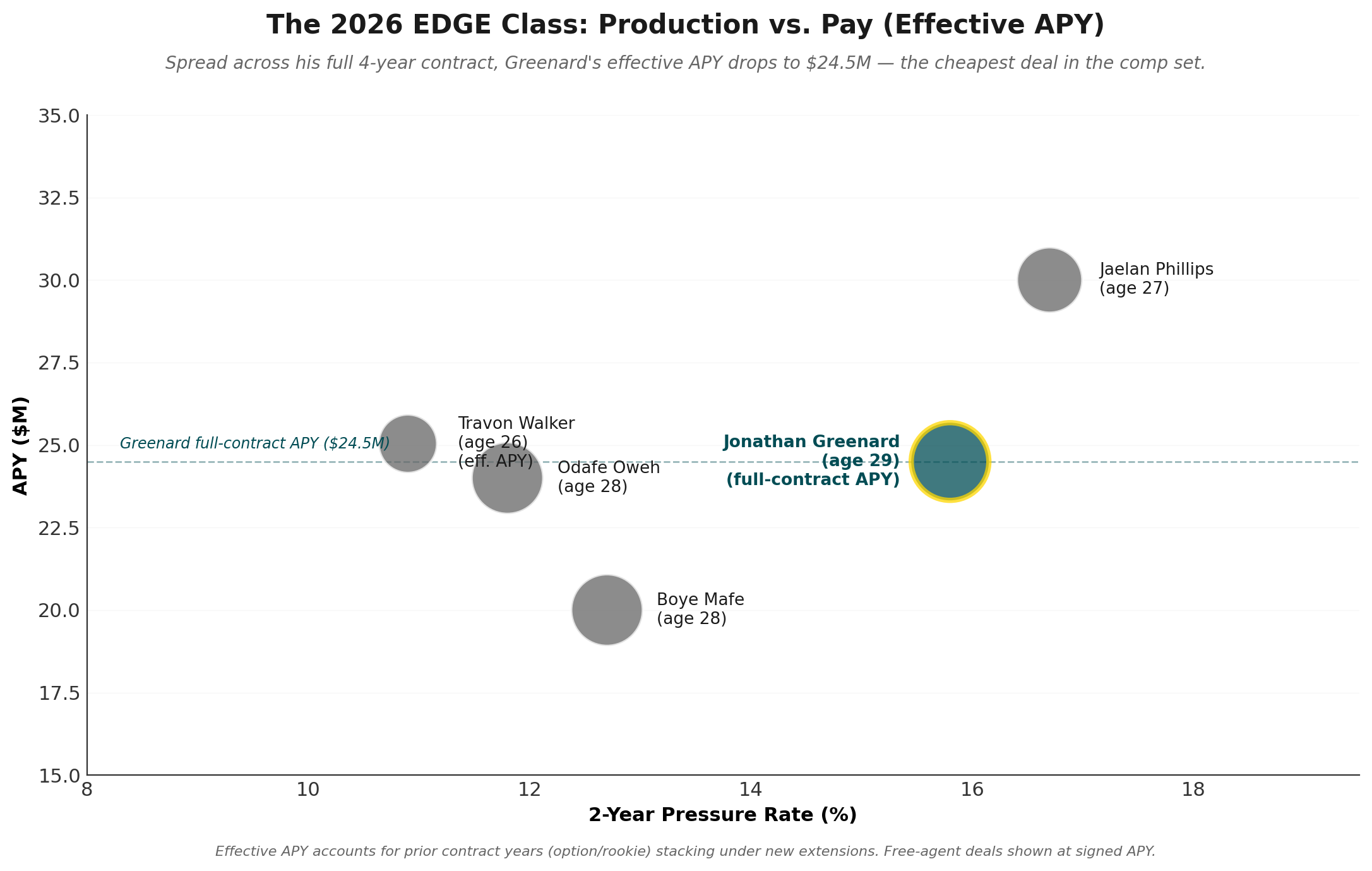

Greenard signed for the same APY as Phillips and more than Travon Walker, Odafe Oweh and Boye Mafe. But that’s new years and new money resulting in the reported APY. What teams care about is the actual years and the cash paid, especially the guaranteed portions. That’s the effective APY. Greenard’s full deal is four years and $98 million. That’s $24.5 million APY. And the Eagles owe him $50 million over 2026 and 2027. That’s a functional APY of $25 million.

Now Greenard’s deal looks much better when working in actualities.

That’s less than Phillips. Less than Walker and Oweh. That’s a solid signing when you consider the pass rush juice upside. The pass rusher market is exploding in real time. Over the past 18 months the market at the mid-to-high end is trending 13% over the entire sample size model. Apply that to the $23.75M APY from my model and his true value locks in at around $26.75M APY.

This does two things. One, it shows even more value that the Eagles picked up in the trade (up to $27.5M in surplus value). And two, it shows that while his extension APY is at a small premium, the effective APY comes in just below his market value. The Eagles found value in the trade and the contract. They won at the margins on both ends of the deal.

Why It Fits the Window

The contract has structural risk. The new-money APY for the two extension years is $30 million, above the comp-adjusted rate. Greenard turns 30 in May of his second contract year. The shoulder injury creates real downside if it lingers. The cash structure makes a clean exit difficult before 2028.

But the window analysis doesn’t care about years three and four. It cares about years one and two.

Those years cover Greenard’s age 29 and age 30 seasons. Those are the two years that align with some of their biggest stars - Saquon Barkley, Dallas Goedert and Lane Johnson. The fully guaranteed $50M is concentrated in exactly those two years. By the time the deal turns into a long-tail risk, the window is closed and the option years protect the team.

Run the Phillips counterfactual and the math gets clearer still. Carolina paid Phillips $30 million APY in March on a four-year, $120 million deal with $80 million guaranteed and $60 million fully guaranteed at signing. Phillips is two years younger than Greenard. But he also has a longer injury history (torn ACL in 2024, ruptured Achilles in 2023). The Eagles tried to retain him but were unwilling to commit to those exorbitant terms. They walked away from a 27-year-old at $30M APY and ended up with a 29-year-old at $24.5M APY whose pre-signing production line matches the player they lost. That is the inverse of an overpay. The trade cost is the price the Eagles paid to escape the bidding war they were losing.

The picks Roseman traded away will produce rookies who would have been useful contributors in 2027 or 2028, by which point the championship window may have closed anyway. Trading 2027 capital for 2026 production is exactly what a contender in its window is supposed to do. Roseman bought two prime years from a top-tier edge rusher, at below-market APY, with a structure that respects the player’s age curve, while also netting roughly $12 - $27.5 million in pure asset surplus on the trade compensation itself.

That’s not the worst deal of the spring. It’s one of the best.

Will Anderson Jr., Houston Texans

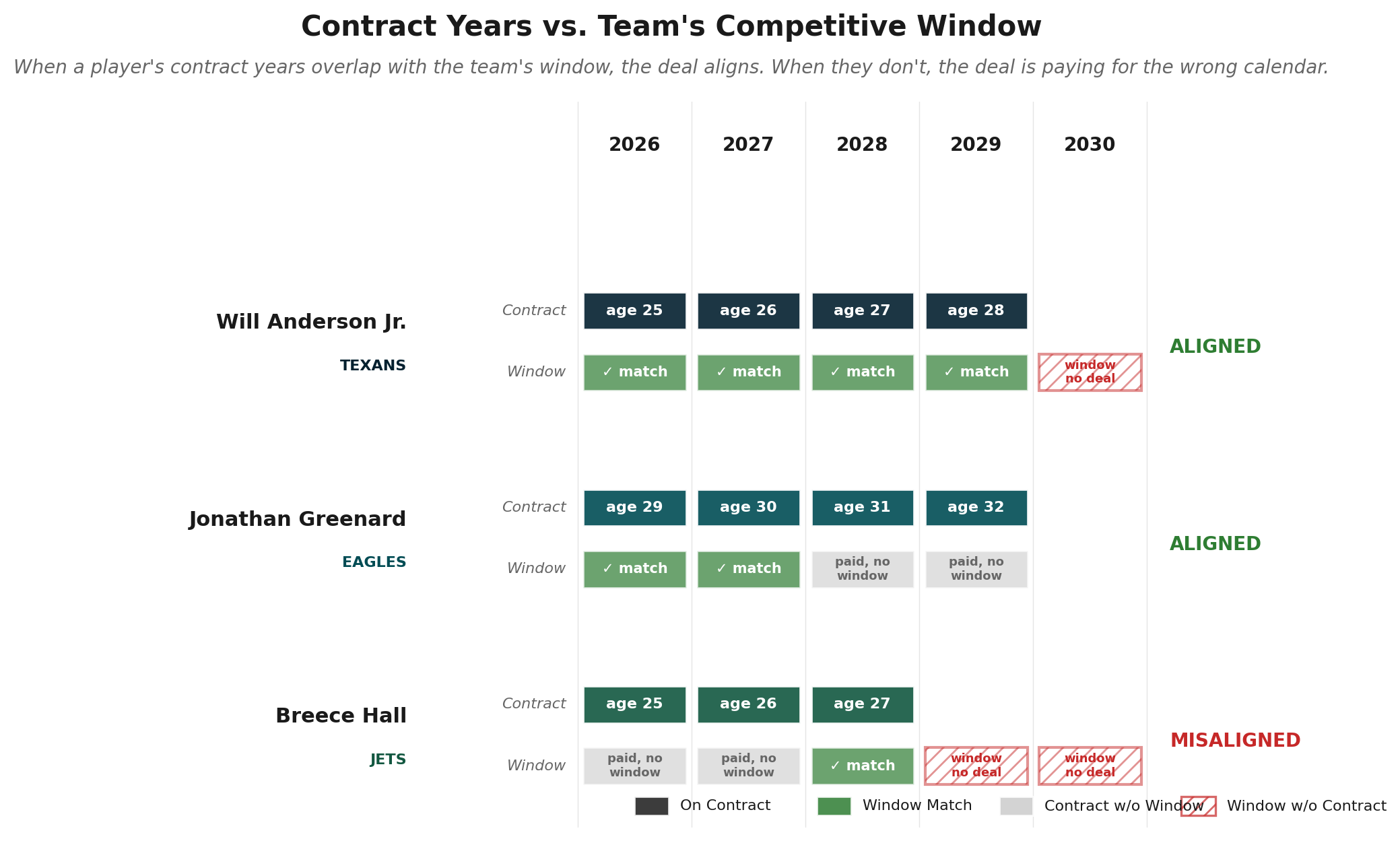

The team timeline: The Texans have made it to the divisional playoff round over the last three seasons only to be bounced before making it further. C.J. Stroud is on a rookie deal through 2027 (the Texans exercised his fifth-year option in April). The defense ranked first in yards allowed and second in points allowed in 2025. Anderson is 24. Anderson and Stroud are a big reason why the roster is built to contend now and continue contending through 2028 and beyond. This is a win-now-and-later franchise with one of the longest credible competitive windows of any team in the AFC.

On April 22, the Texans signed Anderson to a three-year, $150 million extension with $134 million in total guarantees and $100 million fully guaranteed at signing. The extension stacks on top of his fifth-year option, which they had exercised two weeks earlier. He is now under contract through 2030.

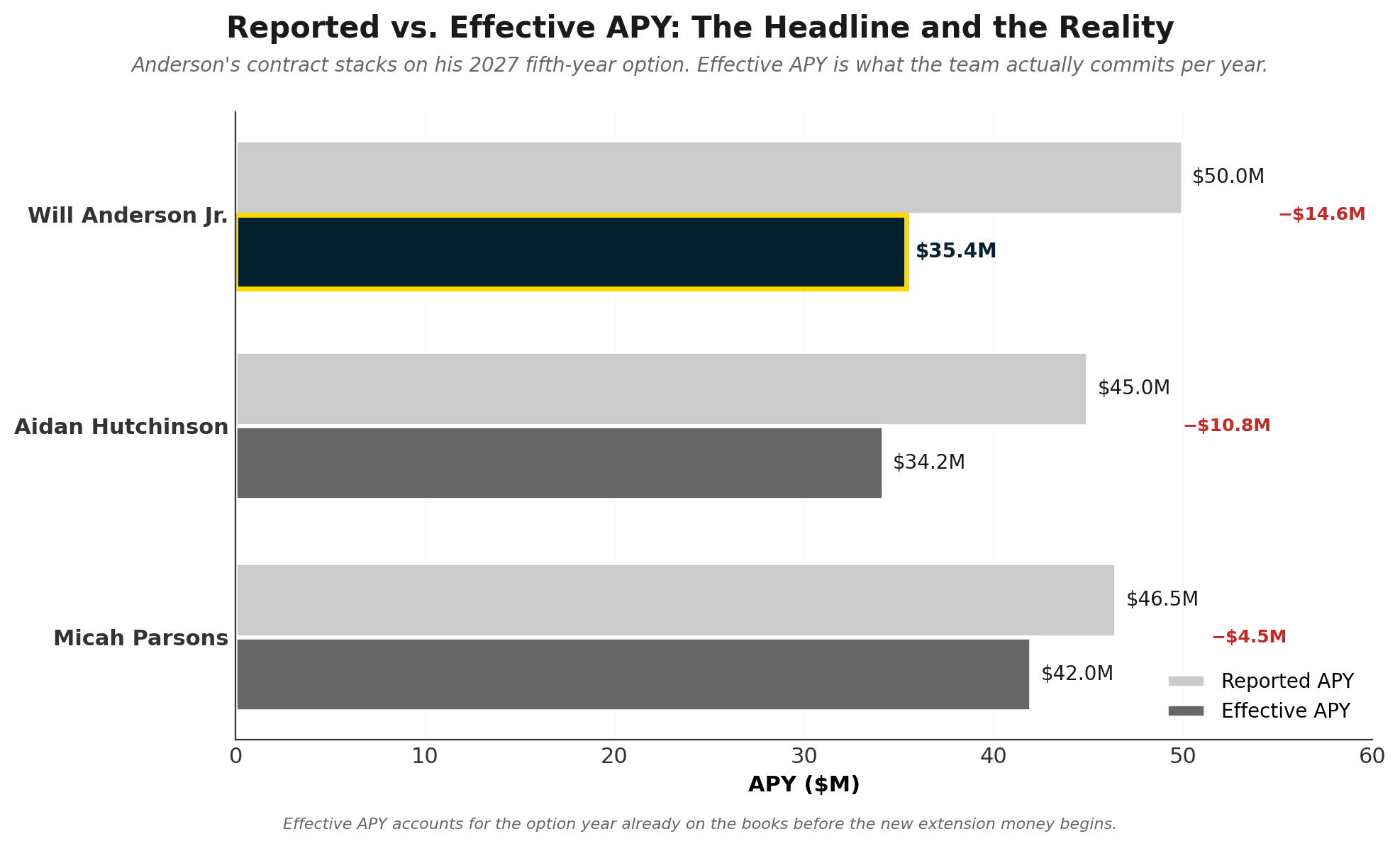

The headline number is what got the attention: $50 million APY, the largest non-quarterback contract in NFL history. By that figure alone, Anderson’s deal sits at the top of the EDGE comp set, above Micah Parsons ($46.5M), Aidan Hutchinson ($45M), and T.J. Watt ($41M).

That number isn’t the right number.

The Effective APY

Anderson’s contract isn’t a true three-year deal at $50M per year. It’s an extension that stacks on top of the 2027 fifth-year option. The Texans’ actual cash commitment from this contract starts with the fourth year of his rookie deal, continues to the option year salary already on the books, and runs through three new years on top.

Run that math properly and the total commitment over five years is $177,063,749. His effective APY is roughly $35.4M, or 11.76% of the 2026 cap.

Compare that to the same calculation for the other top-tier EDGE deals:

Anderson’s effective APY is roughly tied with Hutchinson and well below Parsons. He is not the highest-paid edge rusher in football on a year-by-year cap basis. He is the third highest-paid EDGE when you account for what the Texans are actually committing to per year.

Run his production line through my EDGE model and the blended estimate is $34.16M APY. The tier-adjusted version (applying the 1.20x elite-tier inflation factor) lifts it to $40.99M. Anderson’s effective $35.4M sits almost exactly at the blended estimate and well below the tier-adjusted projection. The model says he should be paid more, not less.

It is true that against the reported $50M APY, the deal carries the largest model premium in the recent EDGE comp set. That premium is a function of contract structure, not market overpay. The reported number is for headlines. The effective number is for analysis.

Why It Fits The Window

Anderson’s effective deal covers his age 25 through 29 seasons, which defines the prime years of an elite edge rusher’s career on average. The Texans bought every season of Anderson’s prime. They are paying market rate once you account for the structure, and they are paying it during a contention window that runs at minimum through Stroud’s 2027 option year and likely several years past that.

The deal works because the timeline works. A win-now-and-later franchise locked in its cornerstone non-QB asset for the entirety of his physical prime, at an effective APY below the model’s tier-adjusted projection, on a defense that just finished as the league’s best. The price is high in headline terms. The fit is exact.

Breece Hall, New York Jets

The team timeline: The Jets finished 2025 at 3-14. Over the course of the 2025 season, they traded their two best defensive players, Sauce Gardner and Quinnen Williams, in moves that signaled a clear pivot to long-term rebuild. Geno Smith, age 36 in 2026, is the bridge quarterback. The 2026 first-round picks were spent on a tight end (Kenyon Sadiq) and a wide receiver (Omar Cooper Jr.). Aaron Glenn and Darren Mougey are in year two of a new regime. Best-case scenarios have the Jets contending in 2027 or 2028, likely with a young quarterback they have not yet drafted.

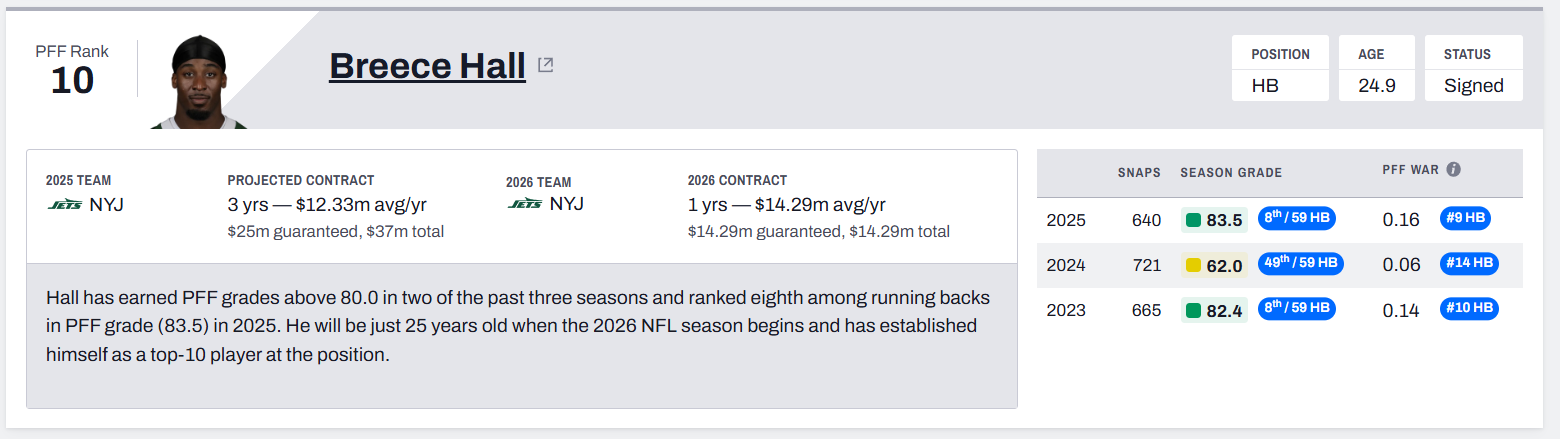

This week, the Jets and Hall agreed to a three-year, $45.75 million extension with $29 million guaranteed. The deal makes Hall the third highest paid running back in football, behind only Saquon Barkley and Christian McCaffrey. He is 24 years old, turning 25 at the end of the month. The contract covers his age 25 through 27 seasons.

The headline read on this deal looks reasonable. A top 10 running back at his absolute physical peak, signed for top three money at the position, on a deal that matches the franchise tag floor for guaranteed cash. Hall is a productive, dual-threat back in a market where the supply of bell-cow running backs is finite. The contract isn’t structurally absurd in isolation.

It’s the alignment that breaks down.

The Two Anchors

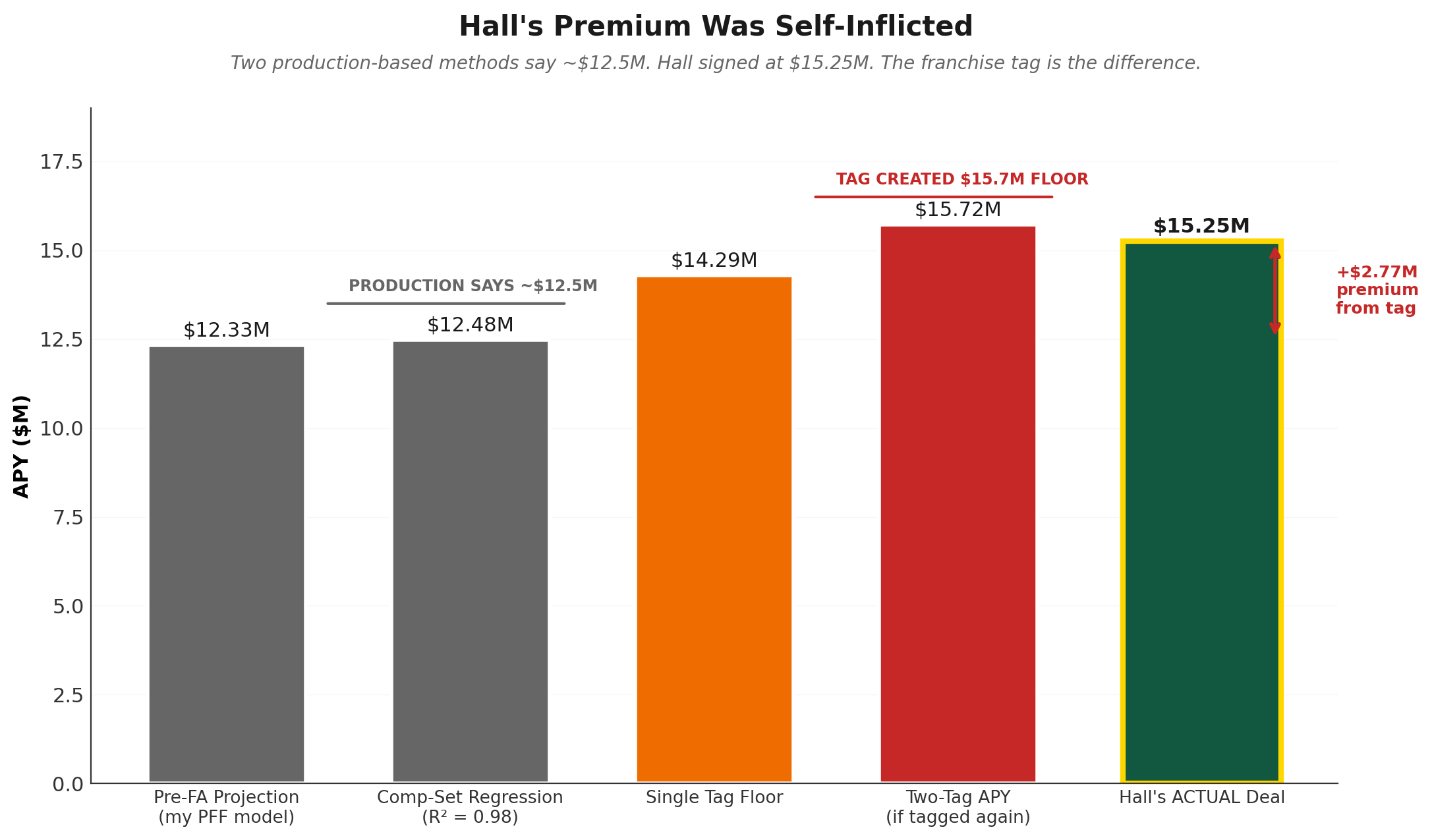

In my work projecting free-agent contracts for Pro Football Focus this offseason, before Hall was tagged and before any of the 2026 RB market had crystallized, my projection on his next contract sat at three years, $37 million, $25 million guaranteed, a $12.33 million APY.

That projection wasn't bearish. It was the natural read of a solid runner who gave three-down upside due to his receiving prowess.

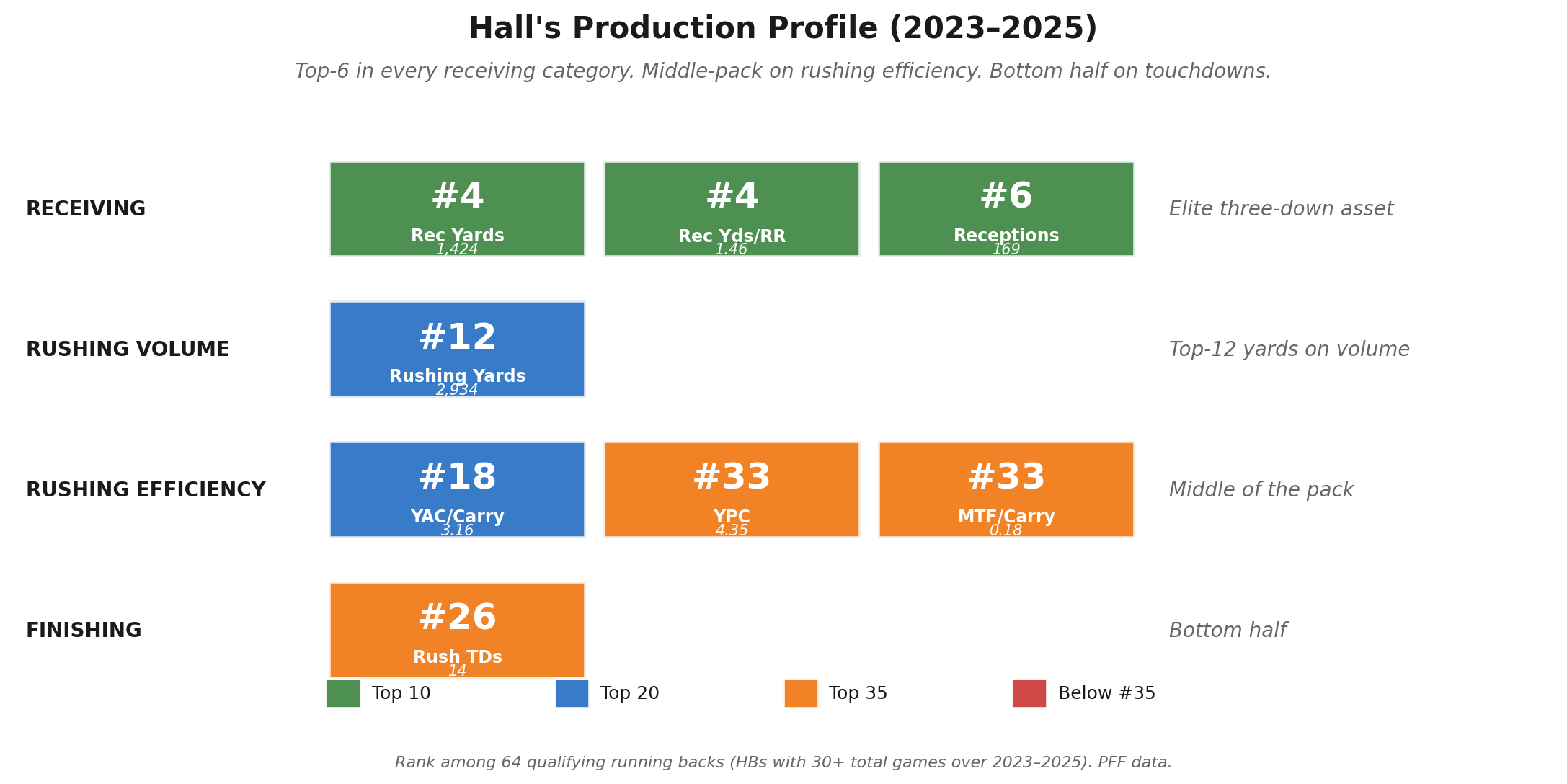

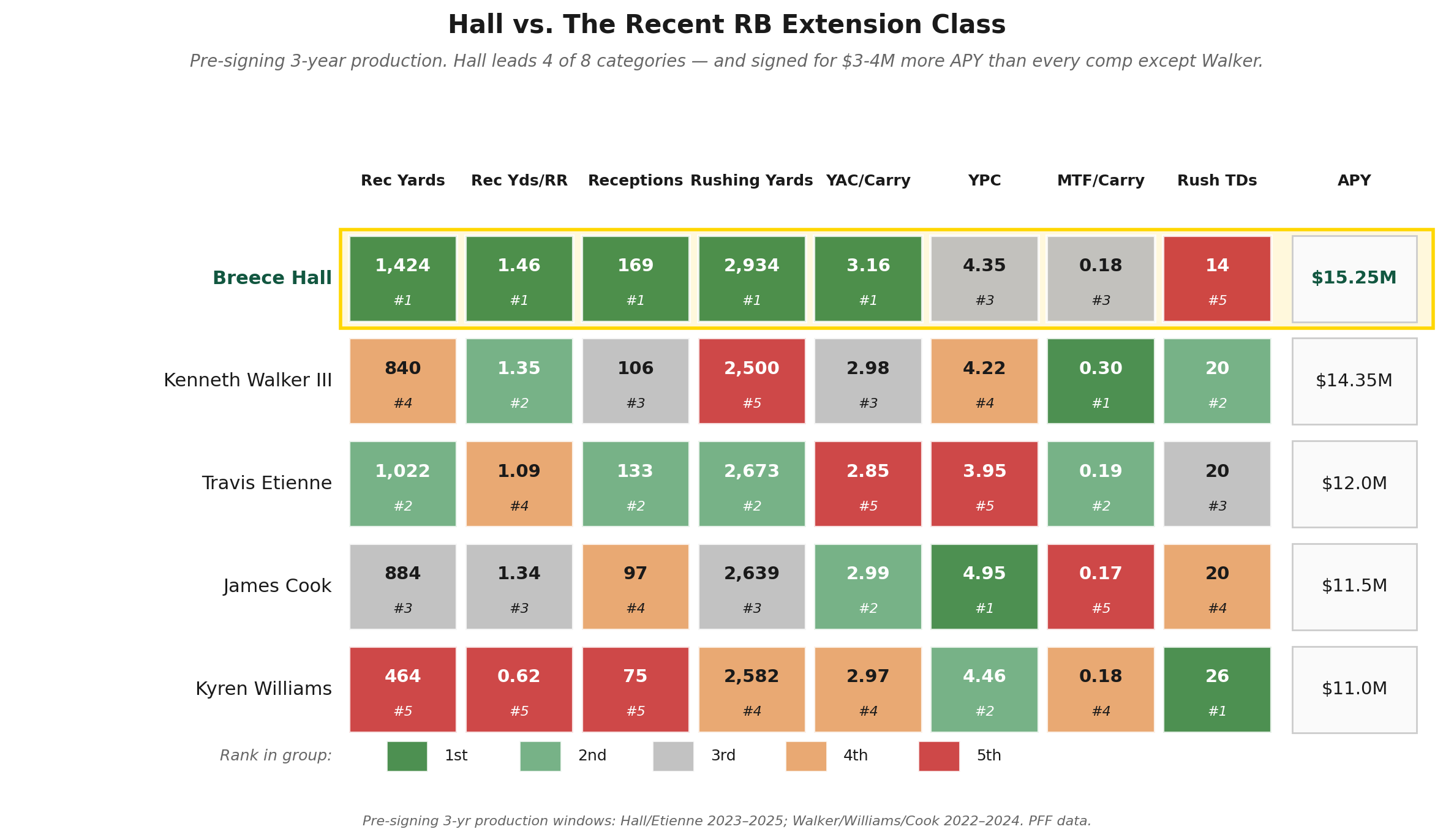

Four other backs have signed in the last 14 months that can provide proper context for Hall: Kenneth Walker III, Kyren Williams, James Cook and Travis Etienne. Look at Hall’s pre-signing 3-year production line against that group and it backs up the original projection I had for him against a larger data set.

The Tag Premium

But Hall’s APY quickly climbed after the Jets placed the franchise tag on him back in March. At $14.293 million, the tag immediately put Hall’s next contract at a premium over his production value.

Once the tag was on, every subsequent negotiation had a different floor. Hall’s representation didn’t have to argue Hall was a $15 million back. They just had to count.

Year one on the tag: $14.293 million, fully guaranteed. Year two on the tag, if applied again, would be 120% of the first tag, or $17.15 million. Across two seasons, that’s $31.44 million in fully-guaranteed-via-tag cash for an APY of $15.72 million. With no negotiation. With no concession on guarantees.

Hall’s actual deal is $15.25M APY with $29M guaranteed at signing, slightly below the two-tag APY but with the security of a multi-year extension and protection against the kind of injury that could have killed a second tag. That’s a rational trade for the player. It’s also, on the surface, a rational trade for the team given the alternative was the same APY with two years of leverage uncertainty.

The thing is: those weren’t the only two options. Without the tag, Hall hits 2026 free agency at the same time Cook and Williams are already locked into sub-$12 million 2025 deals. Walker, Etienne, and Hall would have been the three premium 2026 RB free agents, and the market doesn’t have $15.7 million of guaranteed precedent waiting in the room. Hall in that market lands closer to my $12.33 million pre-FA projection.

The franchise tag didn’t just secure Hall for 2026. It reset the floor of his next contract by roughly $3 million per year.

Why It Doesn't Fit The Window

A $3 million APY premium on a top 10 running back is not the worst deal in football. The Eagles paid above-model APY for Greenard, and the Texans paid full freight for Anderson, and both of those deals work because the contract horizon aligns with a competitive window where premium production matters.

The Jets aren’t there.

Hall’s contract covers his ages 25 through 27. Those are the years the Jets are rebuilding. The team’s actual contention plan looks something like this: develop a young quarterback they don’t yet have, integrate the 2026 first-round picks at tight end and wide receiver, give the new offensive coordinator time to install his system, find replacement-level production at the defensive positions they just sold off in the Gardner and Williams trades, and hope the AFC East thins out enough that a wild card path opens up.

Every one of those things takes time the Jets don’t currently have. By the time the team’s competitive window plausibly opens, sometime around 2028 or later, Hall will be 28 entering 29, on the back half of an RB’s prime, on a contract that no longer has guaranteed money. The team will have spent his most productive seasons getting outscored by good teams while waiting for everything else to come together.

This is what makes the deal misaligned. It’s not that Hall isn’t worth $15 million per year - although it’s a debatable point. It’s that the Jets paid premium money to a position the league has spent years teaching itself to devalue, on a roster that wasn’t ready to convert that production into wins, locking in the player’s prime years for seasons that won’t matter for the team they’re trying to build. Every other position group on the roster has needs. The 2026 free agent class had Cook, Jacobs, and Etienne available at sub-$13M APY before they signed elsewhere. The dollars Hall just absorbed could have funded better talent at guard, cornerback, or any number of other positions on the defense to improve both the ceiling and depth of the team.

The Eagles spent picks and cash on a 29-year-old because their window is now and the player’s two best remaining years align with that window. The Texans spent record money on a 24-year-old because their window runs through 2030 and the player’s entire prime aligns with that window. Both teams used a star player’s contract to extend or maximize a championship window that already existed.

The Jets spent a $3 million annual premium to lock in a 25-year-old’s prime years for a roster that isn’t going to use them. The premium was self-inflicted by the franchise tag application in March. The position was already devalued by half a decade of league-wide cap behavior. The alignment doesn’t work because the math is being applied to a calendar where Hall’s best seasons happen before the team is ready to compete. By the time the Jets are good enough for Hall’s production to matter, his deal is one year from expiring and his best football is two years behind him.

Working through the mechanics and the timeline of each deal, it’s clear why the Eagles are one of the best run organizations in the NFL, why the Texans are on the precipice of that distinction. And why the Jets continue to falter.